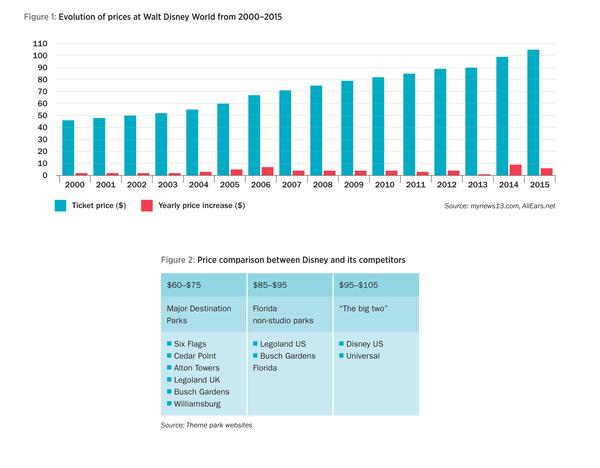

When Disney established its $99 price point in 2014, it could no longer continue to walk in micro-steps towards a perceived $100 “wall” – instead, it had to move the wall. Someone had to do it at some point and, as the market leader, Disney was the logical first mover.

Disney’s bold 2015 pricing decision is supported by historic double-digit growth of underlying financial performance, indicating there’s been no significant resistance to their price points and strategies so far.

A company shouldn’t necessarily be bound by something as artificial as a triple-digit price barrier. It’s not that there isn’t a psychological barrier, but that recent pricing policy at Disney World hasn’t actually had a negative impact on overall park and resort performance.

In taking its pricing decisions, Disney would have looked at its own wealth of internal data as well as broader tourism data and trends and economic indicators, including household expenditure surveys, consumer confidence and much more

In fact, when one compares historical growth of Disney’s lead price against any number of proxy measures and comparables in the US – including leisure services expenditures and pricing for cinema tickets and sports events – Disney’s price growth, is pretty consistent with the upper end of the leisure industry.

Increases in the consumer price index (CPI) tend to be similar over time to inflation – a 2 to 3 per cent average annual growth rate – and overall growth in expenditures for leisure services is just over 3 per cent.

Over 10 and 20-year periods, growth in average cinema ticket pricing is a little higher again, and sports tickets are in the 5 to 8 percent growth rate range. Disney’s lead price growth – at an average annual of 5 to 6 per cent over the same periods, puts Disney towards the upper end of the range, but certainly not as an outlier.

Also important to the Disney pricing policy is the “destination” factor – i.e., hardly anybody pays the walk-up price. Instead, the lion’s share of Disney World’s customers, including international visitors, purchase tickets online, in advance, and typically as part of a multi-day pass and/or package, which offer savings.

A more cynical hypothesis, I suppose, might say that the more you communicate a lofty lead price while simultaneously offering significantly discounted package pricing, the greater the perception of savings by customers. This year’s headline price increased 6 per cent, but multi-day tickets went up between 3 and 4 per cent.

For regional parks, who rely on fixed markets and repeat visitors and face resistance to price rises, there’s an awareness about what Disney’s charging and, as a result, a $62 or $67 lead price at Six Flags or Cedar Fair – which, again due to season passes and promotions, no one really pays – suddenly seems a relatively good deal.

In that way, I suppose it’s fair to say that Disney is pulling the whole train along in terms of the industry’s lead price point.

[email protected]