By the end of 2015, there were a total of 9.3 million people exercising at the leading 20 providers across Europe – an increase of 1.1 million customers (13.3 per cent) compared to the previous year. British and German budget operators show the strongest growth.

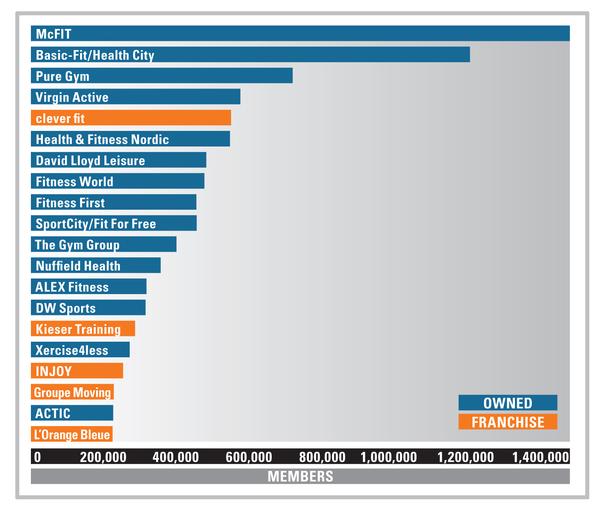

To be listed in the top 20 operators by members, operators needed at least 210,000 members at the end of 2015; to be ranked in the top 10, that figure rose to 430,000 customers (see Figure 1).

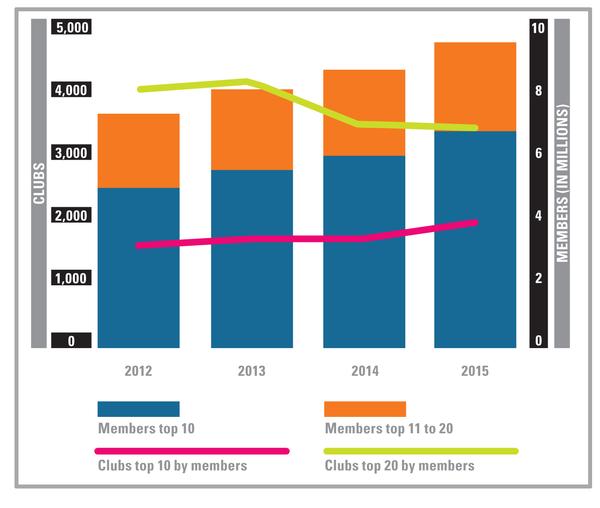

The approximately 3,300 clubs belonging to the top 20 operators hosted on average around 2,800 members each.

TOP PLAYERS BY MEMBERS

The leading fitness company by member numbers remains German budget provider McFIT. Over 1.4 million people currently exercise in the operator’s clubs in Germany, Austria, Poland, Spain and Italy. Germany remains the company’s largest market with 169 clubs. In 2015, McFIT also launched its new concept, High5 – facilities of smaller size and with a price starting at €9.90 – in Germany and Austria.

Second-ranked Basic-Fit/HealthCity group realised a growth of almost 50 clubs over the year and now has more than 1.1 million members. According to media reports, the company – partially owned by private equity firm 3i since 2013 – plans to conduct an IPO later this year. Should this go ahead, it will represent the second big fitness operator IPO in Europe after an absence from European stock exchanges for more than a decade – the first being the successful IPO by British budget operator The Gym Group (11th in the current ranking) at the end of 2015.

The realised valuation of The Gym Group – and the IPO efforts of other providers like Basic-Fit, and SoulCycle in the United States – show that fitness companies seem not only to be of interest to institutional investment companies, but also to investors among the general public.

Meanwhile British operator Pure Gym – which is also rumoured to be considering an IPO – now ranks third with its approximately 700,000 members.

In comparison to last year, the company was able to move up three positions, outstripping established players such as Virgin Active and David Lloyd Leisure.

However, the biggest jump of all came from German franchise provider clever fit: with more than 500,000 members at the end of 2015, it leapt up five places from 10th to fifth in the list.

There are two new providers in the top 20. Xercise4Less, another British budget provider, entered the ranking in 16th place, while franchise offering L’Orange Bleue – which has about 300 clubs, primarily in France – comes in at number 20.

Not included in the top 20 is CrossFit. Although 2,500 CrossFit boxes exist in Europe, they don’t meet the criteria for a fitness club chain due to the pure license payment to CrossFit Inc. Were it included, CrossFit would be ranked in the middle of the top 20, with an estimated total of more than 300,000 members – a significant presence.

MEMBERS UP, LOCATIONS DOWN

Each year, the number of members joining the leading European operators grows. In 2012, the top 10 operators had about seven million members between them; in 2015, that number had surpassed nine million customers (see Figure 2).

The drop in the total number of clubs owned by the top 20 chains was caused by the fact that two small footprint franchise operators left the member-based ranking: Curves (in 2014) and Mrs.Sporty (in 2015) had contributed a relatively high number of clubs compared to traditional providers.

A certain dominance of British operators becomes clear while looking at the geographical origin of the largest chains. Eight of the 20 providers originate from the United Kingdom. In contrast, only three companies are based in Germany. Other countries that are home to the headquarters of more than one top 20 operator are the Netherlands and France, with two companies each.

GROWTH & REVENUE

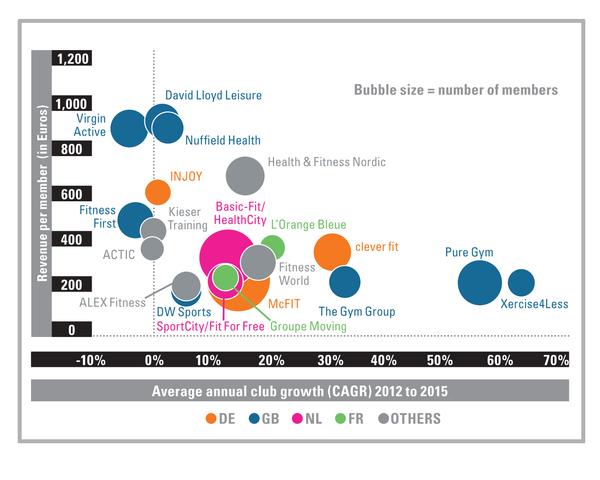

Finally, Figure 3 shows the average annual club growth of the leading providers in relation to the revenue per member; the bubble size corresponds to the number of members at the provider as at 31 December 2015.

When considering this illustration, it becomes clear that especially the British-based budget operators – namely Xercise4Less, Pure Gym and The Gym Group – have been able to increase their number of clubs, with average growth rates of at least 30 per cent per year witnessed among these operators.

They are closely followed by the German budget operator clever fit.

Given the inflow of funds through the aforementioned IPO of The Gym Group, but also the support of financial investors at the remaining British providers, it may be only a matter of time before they dare to make the jump to continental Europe.

Moreover, the 11 fastest growing companies are at least partially active in the budget segment. The significantly higher revenue per member of Health & Fitness Nordic is caused by its higher-priced brand SATS ELIXIA, but its growth was achieved in the Nordic region thanks in part to its budget brand Fresh Fitness.

However, while the top 20 is led by British companies with regard to growth, two other British operators come in at the bottom with the weakest club development performance: both Virgin Active and Fitness First have adjusted their portfolios in recent years and sold individual clubs. Virgin Active found a new investor last year, and media reports suggest that Fitness First could also face a change of ownership.

SHAPE OF THE FUTURE?

It will be exciting to see what 2016 brings, and not only for the leading market players. Will the growth of budget operators continue? How can other operating concepts position themselves in the market? How will small, modern, niche concepts develop further? And what role will investors play in the industry this year?

We will certainly be watching with interest as the story unfolds.